Low Rates.

Our rates are low, our application is quick and easy! We can get you clear to close in as little as 10 days!

Trusted By Agents With

Meet Bill Rapp

NMLS ID # NMLS # 228246

William Rapp, based in Houston, TX, US, is currently a Capital Advisor at Medallion Funds, bringing experience from previous roles at eXp Commercial, NEXA Mortgage, Viking Enterprise LLC and Sun Realty - Houston. William Rapp holds a 1997 - 2001 BBA in Finance @ Texas A&M University. With a robust skill set that includes REO, Sellers, SFR, FHA financing, Reverse Mortgages and more, William Rapp contributes valuable insights to the industry.

The Client Experience

Great experience purchasing our first home! Bill was easy to reach and always able to answer any questions or concerns.

Loan Programs Available

Blogs

The Top 5 Mortgage Mistakes to Avoid

Buying your first home can be both exciting and nerve-wracking at the same time. With so many things to consider and....

Mortgage Do and

Do not list

Mortgages can be tricky, and it's easy to make mistakes that can end up costing you dearly. That's why we've put together this list....

Tips On How To Improve Your Credit Score

Let's talk about some ways you can improve your credit score! Your credit score is actually a big deal, and it can affect...

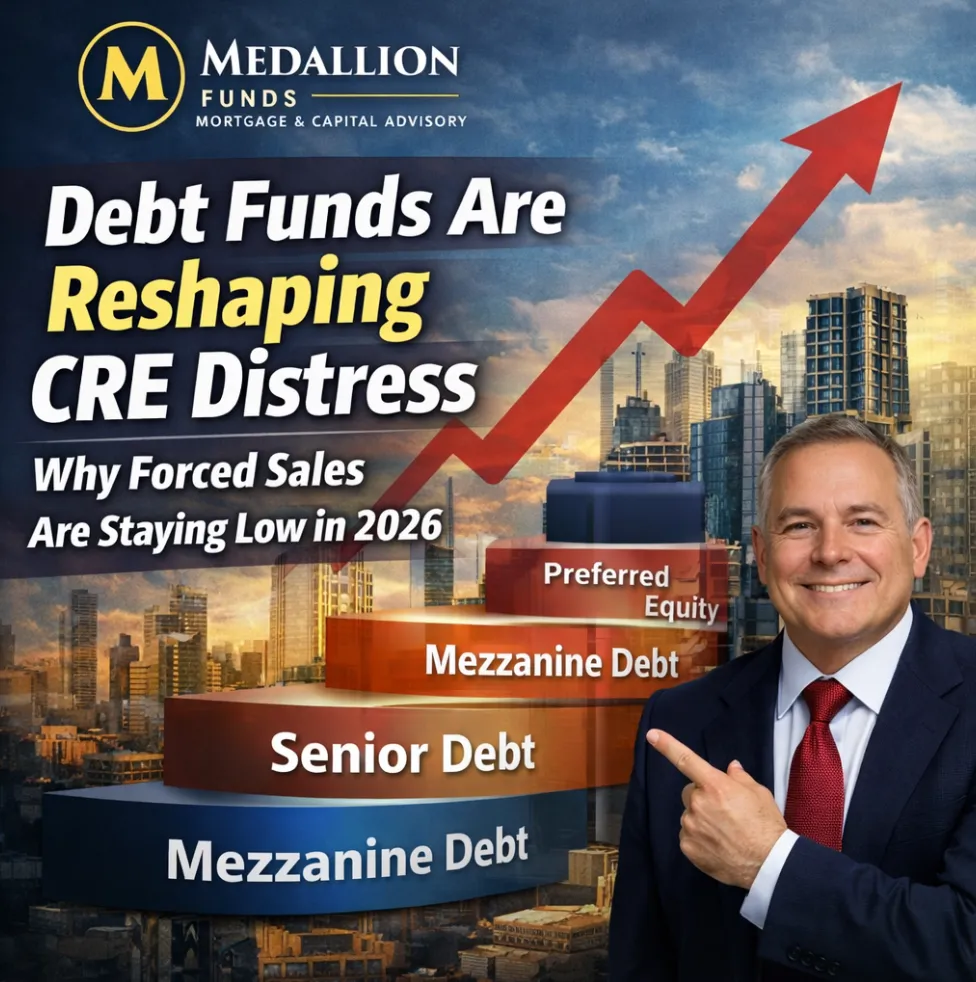

💼 Debt Funds Are Redefining CRE Distress in 2026 📉➡️📈

💼 Debt Funds Are Redefining CRE Distress in 2026 📉➡️📈

🏗️ Why CRE Distress Isn’t Triggering Fire Sales Anymore 💰

Debt Funds and the New Shape of CRE Distress

Commercial real estate distress in the current cycle looks nothing like the aftermath of the Global Financial Crisis. While headlines continue to focus on rising defaults and valuation resets, the data tells a very different story: forced asset sales remain historically low. The primary reason is structural—private debt funds, especially those active in mezzanine lending, have fundamentally reshaped how distress is absorbed and resolved in a positive way.

Distressed Sales Are Historically Muted

Following the Global Financial Crisis, distressed assets represented nearly 20 percent of all commercial property sales by 2010. By comparison, distressed transactions accounted for only about 3 percent of total sales by mid-2025. Even with rising maturity defaults, property values have declined roughly 10 percent this cycle—far less severe than the 23 percent year-over-year correction seen in 2009. Without deep equity impairment, widespread liquidation pressure has simply not materialized.

Private Debt Funds Have Rewritten the Capital Stack

Post-GFC regulatory changes, including HVCRE requirements, significantly reduced banks’ willingness to hold higher-risk construction, bridge, and transitional loans. That void has been filled aggressively by private debt funds. Institutional capital has flowed into these vehicles at scale, giving them flexibility to price risk, structure creatively, and operate across senior, mezzanine, and preferred equity positions.

Market data tracked by MSCI shows a strong correlation between rising dry powder and increased lending activity from these investor-driven lenders. Rather than pulling back during volatility, debt funds have leaned in—providing rescue capital and extension financing that prevents assets from being pushed into forced sales.

Distress Is Concentrated Higher in the Capital Stack

The stress in this cycle is not primarily at the asset level—it is higher in the capital stack. Senior debt performance has remained relatively stable, with income accounting for more than 100 percent of total returns between 2020 and 2025. Mezzanine debt, by contrast, has absorbed significantly more pressure. Losses have pushed income returns above 200 percent, signaling that subordinated capital—not property fundamentals—is where distress is being realized.

Mezzanine Capital Is Reshaping Workouts

Rather than defaulting directly into foreclosure, many sponsors are turning to mezzanine lenders to inject capital and extend runway. These lenders often gain control rights upon default, allowing them to influence recapitalizations, restructures, or sponsor transitions more efficiently. The result is faster resolution, fewer legal delays, and a controlled workout process that preserves asset value.

What This Means for Investors and Borrowers

The modern CRE distress cycle is being resolved through capital restructuring, not mass liquidation. For investors seeking exposure to distress, mezzanine positions often provide faster access to value with greater control and fewer headline risks than traditional foreclosure strategies. For borrowers, understanding the evolving role of debt funds is critical when navigating refinances, extensions, or recapitalizations.

Bottom line: CRE distress hasn’t disappeared—it has moved up the stack. And debt funds are now the primary shock absorbers.

https://www.billrapponline.com/

https://findamortgagebroker.com/Profile/WilliamRappJr28883

https://billrapp.commloan.com/

https://billrapponline.com/financingfuturescre-houston-katy

https://houstoncommercialmortgage.com/

https://author.billrapponline.com

https://doctorvideo.billrapponline.com/

https://veteransvideo.billrapponline.com/

https://mortgageviking.billrapponline.com/

https://fha203h.billrapponline.com/

https://renovationvideo.billrapponline.com

https://medallionfunds.com/bill-rapp/

https://www.amazon.com/dp/B0F32Z5BH2

https://veed.cello.so/FOmzTty6oi9

https://creplaybookseries.billrapponline.com

https://creplaybook.billrapponline.com/

© 2023-2024 Bill Rapp, Medallion Funds LLC, Director of Capital Advisory

10 Tips for First-Time Homebuyers

Buying your first home can be both exciting and nerve-wracking at the same time. With so many things to consider and....

How To Choose the Right Lender for You

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy

Refinancing youe loan and when to do it

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy

Copyright ©2021 | Mortgage Viking Team

Licensed to Do Business | NMLS # 228246

This is not an offer to enter into an agreement. Not all customers will qualify. Information, rates and programs are subject to change without notice. All products are subject to credit and property approval. Other restrictions and limitations may apply. Copyright © 2021 | Medallion Funds

Corporate | NMLS ID NMLS # 1825831

Corporate Address : 2651 N. Green Valley Pkwy STE. 101 Henderson, NV 89014

Corporate NMLS NMLS # 1825831 | Company Website: https://medallionfunds.com/bill-rapp/

Copyright ©2021 | Mortgage Viking Team Licensed to Do Business | NMLS # 228246

This is not an offer to enter into an agreement. Not all customers will qualify. Information, rates and programs are subject to change without notice. All products are subject to credit and property approval. Other restrictions and limitations may apply

Corporate | NMLS ID NMLS # 1825831

Corporate Address : 2651 N. Green Valley Pkwy STE. 101 Henderson, NV 89014 https://medallionfunds.com/bill-rapp/

Facebook

Instagram

X

LinkedIn

Youtube

TikTok