Low Rates.

Our rates are low, our application is quick and easy! We can get you clear to close in as little as 10 days!

Trusted By Agents With

Meet Bill Rapp

NMLS ID # NMLS # 228246

William Rapp, based in Houston, TX, US, is currently a Capital Advisor at Medallion Funds, bringing experience from previous roles at eXp Commercial, NEXA Mortgage, Viking Enterprise LLC and Sun Realty - Houston. William Rapp holds a 1997 - 2001 BBA in Finance @ Texas A&M University. With a robust skill set that includes REO, Sellers, SFR, FHA financing, Reverse Mortgages and more, William Rapp contributes valuable insights to the industry.

The Client Experience

Great experience purchasing our first home! Bill was easy to reach and always able to answer any questions or concerns.

Loan Programs Available

Blogs

The Top 5 Mortgage Mistakes to Avoid

Buying your first home can be both exciting and nerve-wracking at the same time. With so many things to consider and....

Mortgage Do and

Do not list

Mortgages can be tricky, and it's easy to make mistakes that can end up costing you dearly. That's why we've put together this list....

Tips On How To Improve Your Credit Score

Let's talk about some ways you can improve your credit score! Your credit score is actually a big deal, and it can affect...

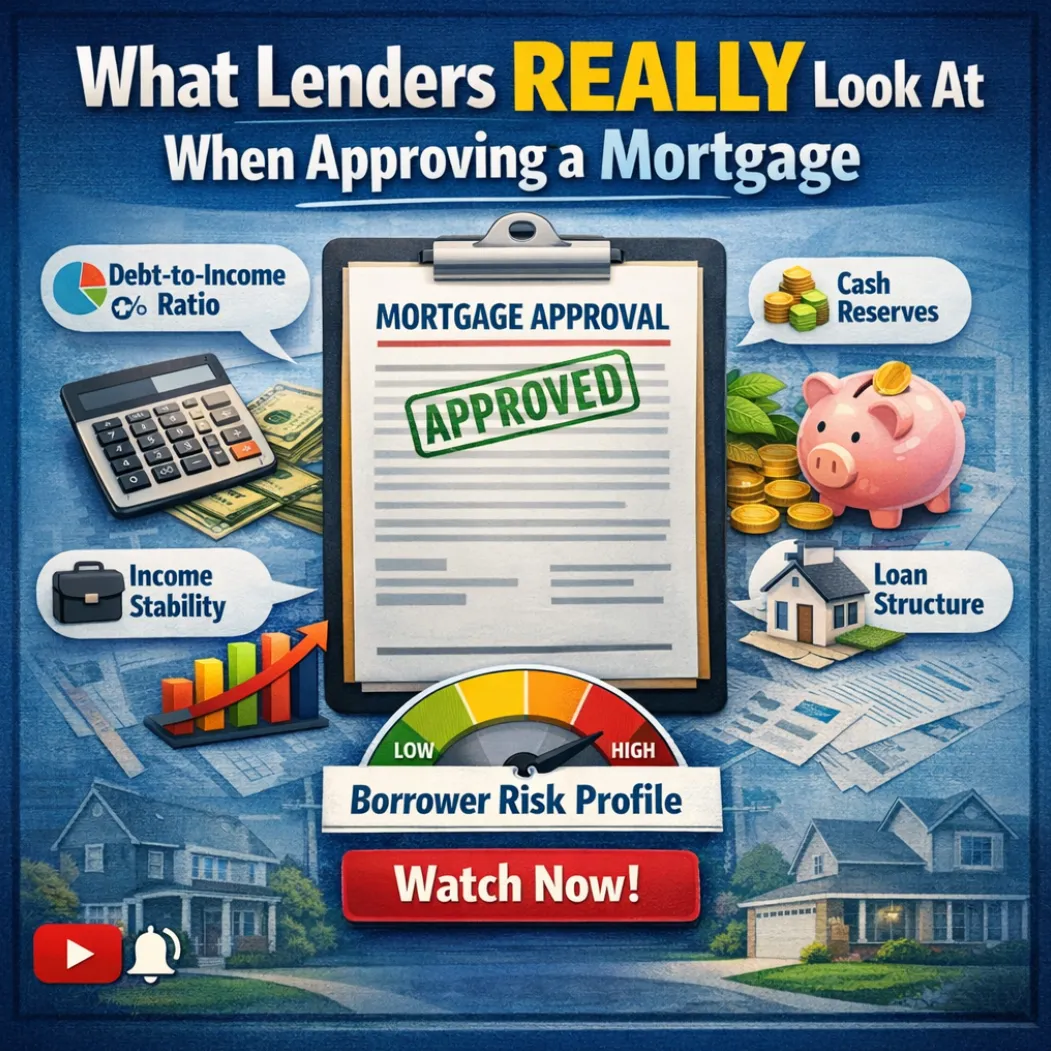

🏦 What Lenders Actually Look At When Approving a Mortgage (Hint: It’s Not Your Credit Score) 🔍

🏦 What Lenders Actually Look At When Approving a Mortgage (Hint: It’s Not Your Credit Score) 🔍

📊 Mortgage Approval Secrets: What Lenders Really Analyze Before Saying Yes 💰

What Lenders Actually Look At (It’s Not What You Think)

Many borrowers assume mortgage approval comes down to three simple numbers: credit score, income, and the interest rate.

But that’s not how lenders actually make decisions.

Behind every loan approval is a much deeper evaluation of risk, structure, and financial stability. In fact, many strong borrowers get denied — not because of credit — but because their financial story doesn’t fit the lender’s model.

Understanding what lenders truly analyze can dramatically improve your chances of approval.

Let’s break down the factors that really matter.

The Biggest Myth: Credit Score Is Everything

Your credit score matters — but it’s not the deciding factor most borrowers believe it is.

Lenders use credit scores primarily as a risk indicator, not as the final approval trigger.

For example:

• A borrower with a 780 score but unstable income may struggle to qualify.

• A borrower with a 690 score but strong cash flow and reserves may get approved easily.

The real question lenders ask is:

“Does this borrower demonstrate financial stability and repayment capacity?”

Factor #1: Debt-to-Income Ratio (DTI)

One of the first things lenders evaluate is Debt-to-Income ratio, or DTI.

This metric compares:

Monthly debt obligations ÷ Gross monthly income

Most traditional mortgage guidelines target:

• 36%–43% DTI for conventional loans

• Up to 50% in some cases with strong compensating factors

But it’s not just the percentage that matters — lenders also analyze debt structure, including:

• Auto loans

• Student loans

• Credit cards

• Personal loans

• Existing mortgages

Strategically restructuring debt can often make the difference between approval and denial.

Factor #2: Income Stability

Lenders are far more concerned with income consistency than income size.

They ask questions like:

• Is the borrower W-2 or self-employed?

• How long have they been in the same industry?

• Is the income stable or seasonal?

For self-employed borrowers, lenders often analyze:

• Two years of tax returns

• Profit trends

• Business stability

This is why bank statement loans and non-QM programs have become increasingly popular — they evaluate actual cash flow instead of tax returns.

Factor #3: Cash Reserves

One factor many borrowers underestimate is liquidity.

Lenders want to see that borrowers have financial reserves available after closing.

Typical reserve expectations include:

• 2–6 months of mortgage payments for primary homes

• 6–12 months for investment properties

Reserves demonstrate financial resilience, which lowers risk for the lender.

Factor #4: Loan Structure

Smart borrowers know something important:

Structure beats rate every time.

A loan with a slightly higher rate but stronger structure can be easier to approve.

Lenders analyze:

• Loan-to-Value (LTV)

• Property cash flow (for investments)

• Collateral strength

• Exit strategy

For investors, lenders often prioritize Debt Service Coverage Ratio (DSCR) rather than personal income.

Factor #5: The Borrower’s Overall Financial Story

Underwriters aren’t just reviewing numbers — they’re evaluating the entire financial narrative.

They want to understand:

• How the property fits into the borrower’s portfolio

• The borrower’s experience

• Risk management strategy

• Long-term repayment capacity

This is where a mortgage broker adds significant value.

Instead of submitting a loan blindly, brokers structure the file so it fits the lender’s risk model.

Why Many Good Borrowers Still Get Denied

Most denials happen for three reasons:

1. Poor deal structure

2. Inconsistent documentation

3. Submitting the loan to the wrong lender

With over 600+ lending sources available today, there is rarely just one solution.

The key is matching the right borrower to the right lender.

Final Takeaway

Mortgage approval is not about finding the lowest interest rate.

It’s about structuring a deal that fits underwriting guidelines and demonstrates stability.

The borrowers who succeed understand that lenders are evaluating:

• Cash flow

• Stability

• Liquidity

• Structure

• Risk management

When those elements align, approvals become significantly easier.

📌 If you're planning to buy, refinance, or invest in real estate, structuring the loan correctly from the beginning can save time, money, and frustration.

https://www.billrapponline.com/

https://findamortgagebroker.com/Profile/WilliamRappJr28883

https://billrapp.commloan.com/

https://billrapponline.com/financingfuturescre-houston-katy

https://houstoncommercialmortgage.com/

https://author.billrapponline.com

https://doctorvideo.billrapponline.com/

https://veteransvideo.billrapponline.com/

https://mortgageviking.billrapponline.com/

https://fha203h.billrapponline.com/

https://renovationvideo.billrapponline.com

https://medallionfunds.com/bill-rapp/

https://www.amazon.com/dp/B0F32Z5BH2

https://veed.cello.so/FOmzTty6oi9

https://buymeacoffee.com/vikingente3

https://creplaybookseries.billrapponline.com

https://creplaybook.billrapponline.com/

© 2023-2024 Bill Rapp, Medallion Funds LLC, Director of Capital Advisory

10 Tips for First-Time Homebuyers

Buying your first home can be both exciting and nerve-wracking at the same time. With so many things to consider and....

How To Choose the Right Lender for You

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy

Refinancing youe loan and when to do it

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy

Copyright ©2021 | Mortgage Viking Team

Licensed to Do Business | NMLS # 228246

This is not an offer to enter into an agreement. Not all customers will qualify. Information, rates and programs are subject to change without notice. All products are subject to credit and property approval. Other restrictions and limitations may apply. Copyright © 2021 | Medallion Funds

Corporate | NMLS ID NMLS # 1825831

Corporate Address : 2651 N. Green Valley Pkwy STE. 101 Henderson, NV 89014

Corporate NMLS NMLS # 1825831 | Company Website: https://medallionfunds.com/bill-rapp/

Copyright ©2021 | Mortgage Viking Team Licensed to Do Business | NMLS # 228246

This is not an offer to enter into an agreement. Not all customers will qualify. Information, rates and programs are subject to change without notice. All products are subject to credit and property approval. Other restrictions and limitations may apply

Corporate | NMLS ID NMLS # 1825831

Corporate Address : 2651 N. Green Valley Pkwy STE. 101 Henderson, NV 89014 https://medallionfunds.com/bill-rapp/

Facebook

Instagram

X

LinkedIn

Youtube

TikTok