The Top 5 Mortgage Mistakes to Avoid

Buying a home can be an exciting and rewarding experience, but it can also be a daunting and overwhelming process, especially for first-time homebuyers.

.

Mortgages are a significant financial commitment, and making mistakes during the process can have serious consequences. In this blog post, we'll explore the top 5 mortgage mistakes to avoid.

1. Failing to Check and Improve Your

Credit Score

Your credit score plays a significant role in determining your eligibility for a mortgage and the interest rate you'll receive. Many first-time homebuyers make the mistake of failing to check their credit score or not taking steps to improve it before applying for a mortgage.

,

To avoid this mistake, check your credit score and take steps to improve it if necessary. This may include paying off outstanding debts, making on-time payments, and disputing any errors on your credit report. A higher credit score can lead to a lower interest rate and a more favorable mortgage offer.

2. Ignoring

Closing Costs

Another common mistake is ignoring closing costs. Many first-time homebuyers are unaware of the various fees associated with closing a mortgage, such as attorney fees, title search fees, and appraisal fees. These costs can add up quickly and significantly impact the total cost of the mortgage.

.

To avoid this mistake, research the average closing costs in your area and budget accordingly. Be sure to factor in these costs when considering the overall cost of the home.

2. Ignoring Closing Costs

Another common mistake is ignoring closing costs. Many first-time homebuyers are unaware of the various fees associated with closing a mortgage, such as attorney fees, title search fees, and appraisal fees. These costs can add up quickly and significantly impact the total cost of the mortgage.

.

To avoid this mistake, research the average closing costs in your area and budget accordingly. Be sure to factor in these costs when considering the overall cost of the home.

3. Not Getting Pre-Approved

Getting pre-approved for a mortgage is an essential step in the home buying process. Pre-approval gives you a clear idea of how much you can afford to spend on a home and helps you avoid the disappointment of falling in love with a home you can't afford.

.

To avoid this mistake, get pre-approved for a mortgage before you start shopping for a home. This will help you narrow down your search to homes that are within your budget and prevent you from wasting time on homes that are out of reach.

4. Taking on Too Much Debt

Taking on too much debt before or during the mortgage process can have serious consequences. Lenders look at your debt-to-income ratio when determining your eligibility for a mortgage. If you have too much debt, you may not qualify for a mortgage or may be offered a higher interest rate.

.

To avoid this mistake, avoid taking on new debt before or during the mortgage process. This includes opening new credit cards, taking out a car loan, or making large purchases on existing credit cards.

4. Taking on Too

Much Debt

Taking on too much debt before or during the mortgage process can have serious consequences. Lenders look at your debt-to-income ratio when determining your eligibility for a mortgage. If you have too much debt, you may not qualify for a mortgage or may be offered a higher interest rate.

.

To avoid this mistake, avoid taking on new debt before or during the mortgage process. This includes opening new credit cards, taking out a car loan, or making large purchases on existing credit cards.

5. Choosing the Wrong Mortgage

Choosing the wrong mortgage can be a costly mistake. There are various types of mortgages available, and each has its pros and cons. Choosing the wrong mortgage can lead to higher interest rates, higher monthly payments, and a more significant financial burden in the long run.

.

To avoid this mistake, research the different types of mortgages available and choose the one that best fits your financial situation and goals. Don't be afraid to ask your lender questions and seek advice from a financial advisor.

Blogs

The Top 5 Mortgage Mistakes to Avoid

Buying your first home can be both exciting and nerve-wracking at the same time. With so many things to consider and....

Mortgage Do and

Do not list

Mortgages can be tricky, and it's easy to make mistakes that can end up costing you dearly. That's why we've put together this list....

Tips On How To Improve Your Credit Score

Let's talk about some ways you can improve your credit score! Your credit score is actually a big deal, and it can affect...

🏠 Where Homes Are (and Aren’t) Affordable in 2025 📉📈

🏠 Where Homes Are (and Aren’t) Affordable in 2025 📉📈

📊 Housing Affordability Crisis: Where Buyers Still Have a Chance 🏡

Where Americans Can’t Afford Homes—And Where Buyers Still Can

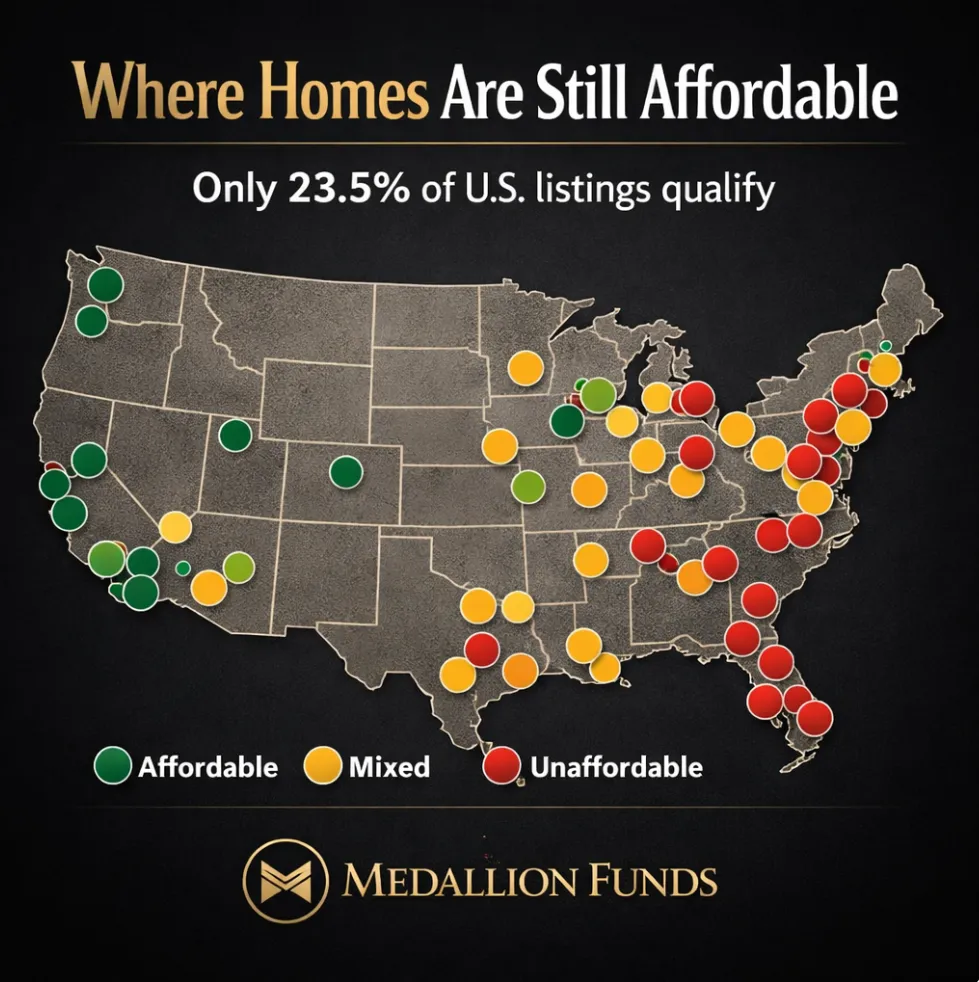

Most Americans cannot afford the homes currently for sale—and where you live matters more than ever.

U.S. housing affordability remains severely constrained. As of July 2025, more than 75% of homes on the market are unaffordable to households earning the national median income of roughly $80,000. Across the 34 largest metro areas, only 23.5% of listings meet standard affordability thresholds.

This isn’t just about mortgage rates. It is the combined effect of elevated home prices, limited housing supply, and uneven construction activity across regions.

📍 Where Homes Are Most Affordable

Affordability improves meaningfully in parts of the Midwest, Rust Belt, and select Southern markets where prices have grown more slowly and supply constraints are less severe.

Markets offering the strongest opportunities for middle-income buyers include:

·Pittsburgh – Approximately 55% of listings affordable

·St. Louis – Roughly 50% affordable

·Baltimore, Detroit, Cincinnati, Birmingham – Around 40% affordable

For buyers willing to be flexible on location—or open to relocating—these markets present realistic ownership paths with standard mortgage structures.

🚫 Where Homes Are Least Affordable

Coastal metros and high-growth Sun Belt cities remain largely inaccessible for median-income households.

Examples include:

·Miami – Just 0.4% of listings affordable

·Los Angeles – Fewer than 2% affordable

·San Diego – Also below 2%

In these markets, price growth has far outpaced income growth, and supply shortages continue to push affordability further out of reach—even for high-earning households.

🧮 Why the Math Doesn’t Work for Most Buyers

This analysis assumes:

·20% down payment

·6.8% 30-year fixed mortgage rate

·Housing costs capped at 30% of gross income

Under those assumptions, the median U.S. home price of $435,000 requires household income of roughly $113,000 per year—about $33,000 above the national median.

This gap explains why many qualified buyers feel “priced out” despite stable employment and strong credit.

🏗️ Supply Is the Real Constraint

Housing supply is diverging sharply by region:

·The South and parts of the West have added inventory through new construction, improving long-term affordability outlooks.

·The Northeast and Midwest remain 40%–60% below pre-pandemic inventory levels, keeping pressure on prices despite slower population growth.

Builders are adapting. Townhomes now account for 18% of single-family construction, nearly double their share a decade ago, making them one of the most important affordability levers for first-time buyers.

🧭 What This Means for Buyers

Even if mortgage rates decline, affordability will not meaningfully improve without sustained increases in housing supply—especially in job-rich, high-demand metros.

This is where mortgage strategy matters. Buyers who understand:

·Market-specific affordability

·Alternative loan structures

·First-time buyer and professional programs

will continue to win—even in constrained markets.

https://www.billrapponline.com/

https://findamortgagebroker.com/Profile/WilliamRappJr28883

https://billrapp.commloan.com/

https://billrapponline.com/financingfuturescre-houston-katy

https://houstoncommercialmortgage.com/

https://author.billrapponline.com

https://doctorvideo.billrapponline.com/

https://veteransvideo.billrapponline.com/

https://mortgageviking.billrapponline.com/

https://fha203h.billrapponline.com/

https://renovationvideo.billrapponline.com

https://medallionfunds.com/bill-rapp/

https://www.amazon.com/dp/B0F32Z5BH2

https://veed.cello.so/FOmzTty6oi9

https://buymeacoffee.com/vikingente3

https://creplaybookseries.billrapponline.com

https://creplaybook.billrapponline.com/

© 2023-2024 Bill Rapp, Medallion Funds LLC, Director of Capital Advisory

10 Tips for First-Time Homebuyers

Buying your first home can be both exciting and nerve-wracking at the same time. With so many things to consider and....

How To Choose the Right Lender for You

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy

Refinancing youe loan and when to do it

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy

🧮 Renovation ROI Calculator

🛠️ Renovation ROI Calculator 💰

Copyright ©2021 | Mortgage Viking Team

Licensed to Do Business | NMLS # 228246

This is not an offer to enter into an agreement. Not all customers will qualify. Information, rates and programs are subject to change without notice. All products are subject to credit and property approval. Other restrictions and limitations may apply. Copyright © 2021 | Medallion Funds

Corporate | NMLS ID NMLS # 1825831

Corporate Address : 2651 N. Green Valley Pkwy STE. 101 Henderson, NV 89014

Corporate NMLS NMLS # 1825831 | Company Website: https://medallionfunds.com/bill-rapp/

Copyright ©2021 | Mortgage Viking Team Licensed to Do Business | NMLS # 228246

This is not an offer to enter into an agreement. Not all customers will qualify. Information, rates and programs are subject to change without notice. All products are subject to credit and property approval. Other restrictions and limitations may apply

Corporate | NMLS ID NMLS # 1825831

Corporate Address : 2651 N. Green Valley Pkwy STE. 101 Henderson, NV 89014 https://medallionfunds.com/bill-rapp/