The Top 5 Mortgage Mistakes to Avoid

Buying a home can be an exciting and rewarding experience, but it can also be a daunting and overwhelming process, especially for first-time homebuyers.

.

Mortgages are a significant financial commitment, and making mistakes during the process can have serious consequences. In this blog post, we'll explore the top 5 mortgage mistakes to avoid.

1. Failing to Check and Improve Your

Credit Score

Your credit score plays a significant role in determining your eligibility for a mortgage and the interest rate you'll receive. Many first-time homebuyers make the mistake of failing to check their credit score or not taking steps to improve it before applying for a mortgage.

,

To avoid this mistake, check your credit score and take steps to improve it if necessary. This may include paying off outstanding debts, making on-time payments, and disputing any errors on your credit report. A higher credit score can lead to a lower interest rate and a more favorable mortgage offer.

2. Ignoring

Closing Costs

Another common mistake is ignoring closing costs. Many first-time homebuyers are unaware of the various fees associated with closing a mortgage, such as attorney fees, title search fees, and appraisal fees. These costs can add up quickly and significantly impact the total cost of the mortgage.

.

To avoid this mistake, research the average closing costs in your area and budget accordingly. Be sure to factor in these costs when considering the overall cost of the home.

2. Ignoring Closing Costs

Another common mistake is ignoring closing costs. Many first-time homebuyers are unaware of the various fees associated with closing a mortgage, such as attorney fees, title search fees, and appraisal fees. These costs can add up quickly and significantly impact the total cost of the mortgage.

.

To avoid this mistake, research the average closing costs in your area and budget accordingly. Be sure to factor in these costs when considering the overall cost of the home.

3. Not Getting Pre-Approved

Getting pre-approved for a mortgage is an essential step in the home buying process. Pre-approval gives you a clear idea of how much you can afford to spend on a home and helps you avoid the disappointment of falling in love with a home you can't afford.

.

To avoid this mistake, get pre-approved for a mortgage before you start shopping for a home. This will help you narrow down your search to homes that are within your budget and prevent you from wasting time on homes that are out of reach.

4. Taking on Too Much Debt

Taking on too much debt before or during the mortgage process can have serious consequences. Lenders look at your debt-to-income ratio when determining your eligibility for a mortgage. If you have too much debt, you may not qualify for a mortgage or may be offered a higher interest rate.

.

To avoid this mistake, avoid taking on new debt before or during the mortgage process. This includes opening new credit cards, taking out a car loan, or making large purchases on existing credit cards.

4. Taking on Too

Much Debt

Taking on too much debt before or during the mortgage process can have serious consequences. Lenders look at your debt-to-income ratio when determining your eligibility for a mortgage. If you have too much debt, you may not qualify for a mortgage or may be offered a higher interest rate.

.

To avoid this mistake, avoid taking on new debt before or during the mortgage process. This includes opening new credit cards, taking out a car loan, or making large purchases on existing credit cards.

5. Choosing the Wrong Mortgage

Choosing the wrong mortgage can be a costly mistake. There are various types of mortgages available, and each has its pros and cons. Choosing the wrong mortgage can lead to higher interest rates, higher monthly payments, and a more significant financial burden in the long run.

.

To avoid this mistake, research the different types of mortgages available and choose the one that best fits your financial situation and goals. Don't be afraid to ask your lender questions and seek advice from a financial advisor.

Blogs

The Top 5 Mortgage Mistakes to Avoid

Buying your first home can be both exciting and nerve-wracking at the same time. With so many things to consider and....

Mortgage Do and

Do not list

Mortgages can be tricky, and it's easy to make mistakes that can end up costing you dearly. That's why we've put together this list....

Tips On How To Improve Your Credit Score

Let's talk about some ways you can improve your credit score! Your credit score is actually a big deal, and it can affect...

📉 CRE CLO Distress Hits 2025 Low — But Maturity Defaults Are Exploding 🚨

📉 CRE CLO Distress Hits 2025 Low — But Maturity Defaults Are Exploding 🚨

🏦 CRE CLO Market Rebounds in 2025 — Even as Non-Performing Maturities Surge ⚠️

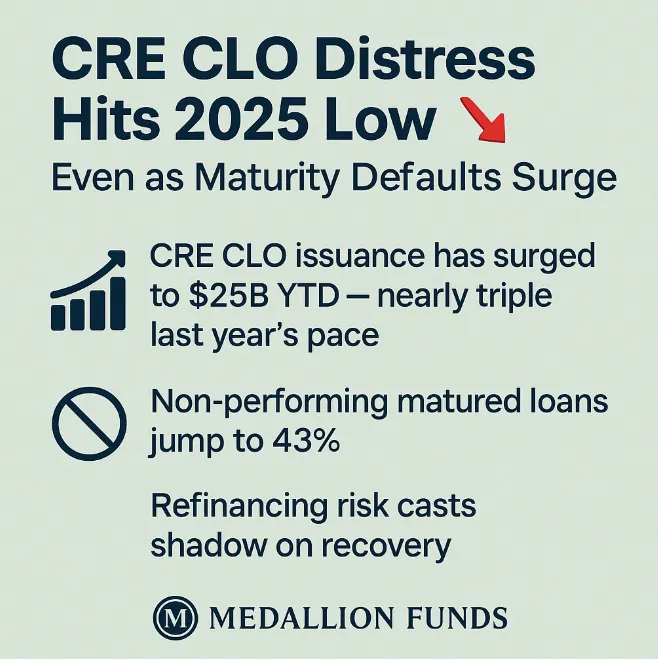

📉 CRE CLO Distress Hits 2025 Low — Even as Maturity Defaults Surge

The CRE debt markets are sending mixed messages as we close out 2025. On the surface, distress levels inside the CRE CLO sector have continued to improve. But beneath the headline optimism lies a growing concern: a surge in non-performing matured loans that is now dominating lender attention, underwriting conversations, and refinance strategies.

As a mortgage brokerage serving commercial investors nationwide, Medallion Funds helps borrowers navigate these shifting conditions — and today’s data tells a story every investor and operator should be watching closely.

📈 CRE CLO Issuance Surges as the Market Reopens

CRE CLO issuance has roared back to life. Through November 2025, total issuance hit $25 billion YTD, nearly triple the $8.7 billion pace from this time last year.

This rebound signals:

·A return of risk appetite among lenders

·Improved liquidity for bridge and transitional assets

·Investor confidence in sponsors with strong business plans

But the healthier issuance volume tells only half the story.

📉 Distress Levels Hit 2025 Lows — A Real Sign of Stabilization

According to CRED iQ:

·The distressed rate fell to 10.7% in October,

·Down 82 bps month-over-month,

·And down 144 bps year-over-year.

CRE CLO delinquencies improved as well:

·8.5% in October, down from 9.2%

However, special servicing inched up to 7.3%, proof that many properties still face cash-flow or business-plan issues requiring active workout strategies.

This is the contradiction of today’s market: distress is falling, but risk is rising.

🚨 The Real Threat: Non-Performing Matured Loans Spike to 43%

The most concerning trend is the rapid growth in non-performing matured loans:

·Jumped 720 bps to 43.0%

·66.3% of all allocated loan balances are now matured

o23.3% performing maturities

o43.0% non-performing maturities

Meanwhile:

·Current loans dropped to 18.2%

·Short-term delinquencies rose from 0.5% → 2.5%

This is the maturity wall in full effect.

Borrowers who took 2021–2022 floating-rate bridge loans are struggling to refinance into a market with:

·Lower valuations

·Higher debt yield requirements

·Tighter DSCR minimums

·Reduced lender leverage

Even with rate relief, the refinancing gap is widening.

🏦 What This Means for Investors, Sponsors & Lenders

The story going into 2026 is simple:

Headline distress is improving… but maturity risk is the real storm.

Borrowers must now:

·Reposition their assets faster

·Shore up NOI

·Inject fresh equity

·Prepare recapitalization strategies

·Move early on refinancing

Lenders, including Medallion Funds’ 600+ capital partners, are already adjusting underwriting around:

·Reduced leverage

·Tighter DSCR overlays

·Greater scrutiny of trailing-12 cash flow

·More conservative ARVs on transitional assets

The borrowers who win in 2026 will be those who prepare before maturity — not after.

💡 How Medallion Funds Helps Borrowers Navigate the Maturity Wall

We assist investors by:

·Running refinance stress tests

·Modeling exit DSCR + valuation scenarios

·Matching borrowers to bridge, bank, debt fund, or private capital

·Structuring rescue capital when needed

·Managing lender communications + underwriting

Whether you’re navigating a 2025/2026 maturity or preparing to acquire transitional assets, planning early is essential.

Final Takeaway

The improvement in CLO distress rates is real — but the surge in non-performing maturities is the bigger, more consequential story.

For investors, the opportunity is clear: transitional assets with strong operators and the right capital stack will be the big winners of the next cycle.

For borrowers, the message is even clearer: prepare now, before your refinance becomes a crisis.

https://www.billrapponline.com/

https://findamortgagebroker.com/Profile/WilliamRappJr28883

https://billrapp.commloan.com/

https://billrapponline.com/financingfuturescre-houston-katy

https://houstoncommercialmortgage.com/

https://author.billrapponline.com

https://doctorvideo.billrapponline.com/

https://veteransvideo.billrapponline.com/

https://mortgageviking.billrapponline.com/

https://fha203h.billrapponline.com/

https://renovationvideo.billrapponline.com

https://medallionfunds.com/bill-rapp/

https://www.amazon.com/dp/B0F32Z5BH2

https://veed.cello.so/FOmzTty6oi9

https://creplaybookseries.billrapponline.com

https://creplaybook.billrapponline.com/

© 2023-2024 Bill Rapp, Medallion Funds LLC, Director of Capital Advisory

10 Tips for First-Time Homebuyers

Buying your first home can be both exciting and nerve-wracking at the same time. With so many things to consider and....

How To Choose the Right Lender for You

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy

Refinancing youe loan and when to do it

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy

🧮 Renovation ROI Calculator

🛠️ Renovation ROI Calculator 💰

Copyright ©2021 | Mortgage Viking Team

Licensed to Do Business | NMLS # 228246

This is not an offer to enter into an agreement. Not all customers will qualify. Information, rates and programs are subject to change without notice. All products are subject to credit and property approval. Other restrictions and limitations may apply. Copyright © 2021 | Medallion Funds

Corporate | NMLS ID NMLS # 1825831

Corporate Address : 2651 N. Green Valley Pkwy STE. 101 Henderson, NV 89014

Corporate NMLS NMLS # 1825831 | Company Website: https://medallionfunds.com/bill-rapp/

Copyright ©2021 | Mortgage Viking Team Licensed to Do Business | NMLS # 228246

This is not an offer to enter into an agreement. Not all customers will qualify. Information, rates and programs are subject to change without notice. All products are subject to credit and property approval. Other restrictions and limitations may apply

Corporate | NMLS ID NMLS # 1825831

Corporate Address : 2651 N. Green Valley Pkwy STE. 101 Henderson, NV 89014 https://medallionfunds.com/bill-rapp/